Brexit happened on 31st December 2020 and many commentators felt there was a lack of clarity in the advice given to businesses. On the 8th April, 2021 HMRC updated the wording and the advice notes on some but not all of the 9 boxes on the UK VAT return. This is to attempt to clarify things that have changed post-Brexit, in particular, the use of the new postponed VAT accounting (PVA) and also the new rules around Northern Ireland due to the Northern Ireland Protocol.

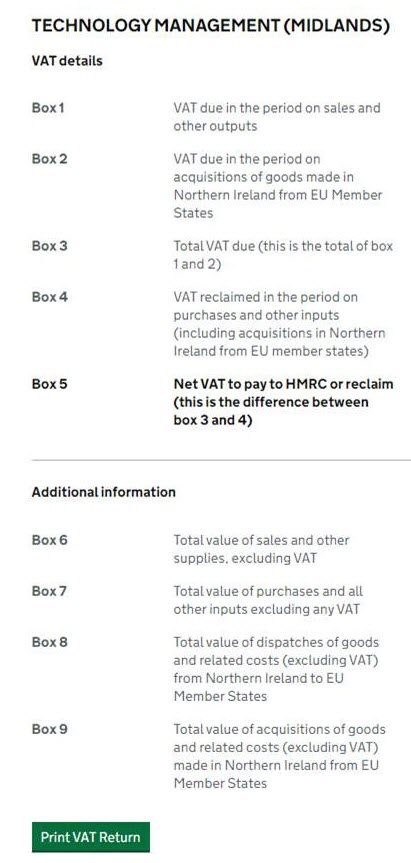

• Boxes 2,4,8 and 9 have had their wording (and the advice notes) changed.

• Boxes 1,3,4,5,6 and 7 have not had their wording changed, but the advice notes have been updated to include reference to post Brexit changes like PVA

• Most of the wording changes actually are the adding in of a reference to Northern Ireland with regard to EU sales or acquisitions.

• Boxes 8 and 9 are now only used if you have supplied goods to or acquired goods from an EU member state under the Northern Ireland Protocol.

This link explains how it works https://www.gov.uk/guidance/how-to-fill-in-and-submit-your-vat-return-vat-notice-70012

It means you need to change how your VAT Statement is set up in Microsoft Dynamics 365 Business Central or Microsoft Dynamics Nav (yes again, sorry). You will need to make a minor change to the totalling so that your post-Brexit EU sales and purchases do not display in Boxes 8 and 9 but do continue to be included in Boxes 6 and 7.

It might be a good idea to go into the VAT Statement that you are using and update the wording there, so you have the current wording as a reference when doing checks on your return.

The change to Boxes 2 and 4 is simply clarifying that only NI-EU or EU-NI goods transactions still use the reverse charge VAT process, our customers that have amended their setup to stop using the EU Reverse Charge process need to take no further action with those boxes. But check you have done this.

The change to Boxes 8 and 9 will require action, as at the time of Brexit there had been no such clarification from HMRC re the use of these boxes, so we went with continuing the existing usage until told otherwise.

All of the above assumes you are a mainland UK VAT registered business. For a business established in Northern Ireland then these boxes 8 and 9 are relevant in the same way that the Intrastat and EC Sales list reporting requirements continue, due to the Northern Ireland Protocol.

However, if the business operates from multiple locations, with some warehouses in NI and some warehouses in mainland UK it will be necessary to distinguish EU-NI and NI-EU goods movements from UK-EU and EU-UK goods movements, as only the former should be on the EC Sales List, the Intrastat report if applicable and now Boxes 8 and 9 on the Vat Return.

So, if you are sat there thinking I have just done my VAT return and it had figures in Boxes 8 and 9 that I now think should not be there, well you won’t be alone as these changes have not been well publicised.

The short answer is to take advice, refer to your accountants/VAT advisors. You could ring HMRC and ask. You may feel it is appropriate to submit a VAT652 form. Taking the example of figures in Boxes 8 and 9 that should not be there, this doesn’t affect the final amount in Box 5 that you pay or reclaim, so your VAT is correct but the additional information section is not and you may be advised to submit a correction for this so there is no confusion from other departments (i.e. those dealing with Intrastat).

We have included an image of the new wording taken from the Government Gateway.

The previously mentioned link to VAT Notice 700/12 does explain things, but you need to read it carefully and it's really section 3 that we need HERE.

Rather than repeat the work of others, there are some good summaries available, including THIS summary from an accountancy firm and THIS from Sage.

We hope this information is helpful to you, if you need further help then please contact your Tecman Account Manager to arrange assistance.